Volume 35: Paper 3

Implications of Monetary Policy Shocks on Consumption with Inflation Expectations

Emma Leonard

єЪБПІ»ґтмИ

emmaa.leonard@gmail.com

Javohn Dyer-Smith

Michigan State University

dyersmit@msu.edu

Consumer spending decisions are central to the functioning of the U.S. economy. В Households continuously allocate resources across necessities, discretionary goods, and services while forming expectations about future economic conditions. These expectations influence not only current spending decisions but also broader macroeconomic outcomes such as inflation, unemployment, and production.

The recent surge in inflation renewed interest in how consumers respond to monetary policy actions. Inflation reached 9.1 percent in July 2022, the highest rate in decades, before gradually declining toward 3 percent by mid-2024. Elevated inflation created substantial uncertainty for households and policymakers alike, particularly because inflation remained persistent despite contractionary monetary policy. This environment highlighted the importance of understanding how monetary policy shocks shape inflation expectations and alter consumption behavior across sectors.

Traditional macroeconomic models often assume highly rational and uniform responses to monetary policy. However, consumers may react differently across categories of spending depending on the durability, necessity, and financing requirements of goods and services. Durable goods purchases, for example, can often be postponed and are highly sensitive to interest rates, while nondurable goods and many services are more closely tied to everyday consumption needs.

This paper empirically examines how monetary policy shocks affect personal consumption expenditures in durable goods, nondurable goods, and services. We employ an instrumental variable vector autoregression (IV-VAR) methodology following Bauer and Swanson (2022). The IV-VAR approach combines vector autoregression modeling with externally identified monetary policy shocks derived from high-frequency financial market reactions surrounding Federal Reserve announcements. This methodology provides a more exogenous identification strategy and reduces contamination from broader macroeconomic conditions already known by market participants.

Our findings show that durable goods consumption exhibits the strongest response to monetary policy shocks despite services accounting for the largest share of total PCE. Inflation expectations also respond sharply following shocks before gradually stabilizing. These results suggest that consumer expectations and sectoral spending characteristics play an important role in the transmission of monetary policy.

The remainder of the paper is organized as follows. Section I reviews the relevant literature. Section II describes the data. Section III outlines the empirical methodology. Section IV presents the results, and Section V concludes.

I. Background

Inflation and inflation expectations are critical determinants of macroeconomic stability. Anchored long-term inflation expectations allow central banks to effectively pursue price stability, and in the case of the Federal Reserve, maximum employment. When households and firms believe inflation will remain near the Federal Reserve’s target, temporary shocks are less likely to generate persistent inflationary spirals.

The Federal Reserve has historically influenced inflation expectations through credible monetary policy communication and consistent inflation targeting. During the high inflation period of the 1970s, inflation expectations became unanchored, contributing to sustained increases in realized inflation. In contrast, inflation expectations remained relatively stable during the 2000s despite rising oil prices, suggesting stronger confidence in the Federal Reserve’s commitment to maintaining price stability.

Behavioral economics also plays an important role in shaping inflation expectations. Tversky and Kahneman (1973) describe the availability heuristic, where individuals rely on highly visible or memorable price changes when forming expectations. Armantier et al. (2011) further demonstrate how consumers often rely on information that is easier and less costly to interpret, such as grocery prices or gasoline prices, rather than formal inflation statistics released by government agencies.

Previous literature also highlights the importance of monetary policy transmission through expectations. Diegel and Nautz (2021) show that long-term inflation expectations significantly influence the effects of monetary policy on inflation and unemployment. Similarly, McKay et al. (2016) argue that market imperfections and financial constraints alter the effectiveness of forward guidance.

Although existing research examines inflation expectations and monetary policy transmission separately, fewer studies investigate how monetary policy shocks affect sector-specific consumption patterns through the expectations channel. This paper contributes to the literature by examining heterogeneous responses across durable goods, nondurable goods, and services using modern external instrument techniques.

II. Data

Our IV-VAR model includes five monthly variables measured from 1988 to 2017: industrial production, the three-month real interest rate, inflation expectations, unemployment, and personal consumption expenditures (PCE).

Personal consumption expenditure (PCE) data were obtained from the Bureau of Economic Analysis (BEA), which provides a comprehensive measure of household spending across the U.S. economy. To better examine heterogeneous consumption responses, we separate PCE into three major categories: durable goods, nondurable goods, and services. Durable goods include longer-lived items such as vehicles, furniture, and appliances, which are often financed and highly sensitive to interest rates and economic expectations. Nondurable goods consist of shorter-lived and frequently purchased items such as food, clothing, and household supplies. Services include expenditures on healthcare, housing services, transportation, recreation, and other non-tangible forms of consumption. This sectoral breakdown allows us to evaluate whether monetary policy shocks produce asymmetric effects across different forms of consumer spending.

Industrial production data were collected from the Federal Reserve Board of Governors and serve as a proxy for aggregate productive economic activity in the manufacturing, mining, and utility sectors. Because industrial production is highly responsive to changes in economic conditions, it provides insight into the broader real-side effects of monetary policy shocks. Unemployment data were obtained from the Bureau of Labor Statistics (BLS) and capture labor market responses following changes in monetary conditions. The three-month real interest rate was constructed using short-term Treasury yield data and reflects short-run borrowing costs faced throughout the economy. This variable is particularly important in identifying the transmission of contractionary or expansionary monetary policy into financial conditions.

Inflation expectations were measured using the University of Michigan Surveys of Consumers, which provide widely used household-level expectations regarding future inflation. Inflation expectations are a central component of modern monetary theory because they influence both current spending behavior and future price-setting decisions. Consumers who expect higher future inflation may accelerate purchases in the present, particularly for durable goods, while expectations of declining inflation may suppress current consumption. Incorporating expectations into the model therefore provides a more comprehensive understanding of how monetary policy influences household behavior.

Lastly, we employ the monetary policy shock developed by Bauer and Swanson (2022) as the external instrument. We use their orthogonalized high-frequency monetary policy surprise series directly without modification. This approach isolates the exogenous component of monetary policy shocks by removing information correlated with publicly available macroeconomic and financial data.

III. Methodology

Recent literature questions whether conventional monetary policy surprises are fully exogenous because financial markets may anticipate policy decisions using publicly available information. To address this issue, we employ the external instrument methodology proposed by Bauer and Swanson (2022), which utilizes orthogonalized high-frequency monetary policy shocks surrounding Federal Reserve communications.

The reduced-form VAR is specified as:

$$Y_t= ОІ_1Y_{t-1}+ОІ_2Y_{t-2}+…+ОІ_pY_{t-p}+u_t$$

where the vector, Yt, includes industrial production, the real interest rate, inflation

expectations, unemployment, and sector-specific PCE measures (durables, nondurables, or services). As the monetary policy shock is already defined, the interest rate variable is shocked and incorporated into the Yt vector in a two stage process.

Impulse response functions (IRFs) are then estimated to evaluate the dynamic responses of each variable following a monetary policy shock. Bayesian estimation methods are used following Miranda-Agrippino and Ricco (2021).

For each structural shock eit:

В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В В IRF(h) = О¦hCi

Where О¦h are the moving average coefficients derived from the VAR model. We estimate the model with Bayesian estimation, as done by Miranda-Agrippino and coauthors (2019).

IV. Results

Using the external instrument VAR methodology, we investigate the dynamic responses of key economic indicators to shocks in PCE across three categories: durables, nondurables, and services. The impulse response functions are reported for 36 periods, which is 3 years after the shock hits, and provides detailed insights into how these shocks propagate through the economy.

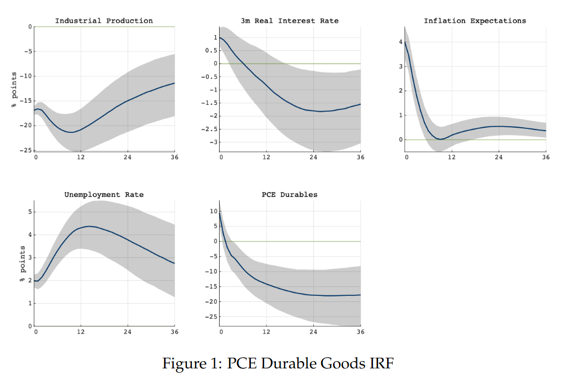

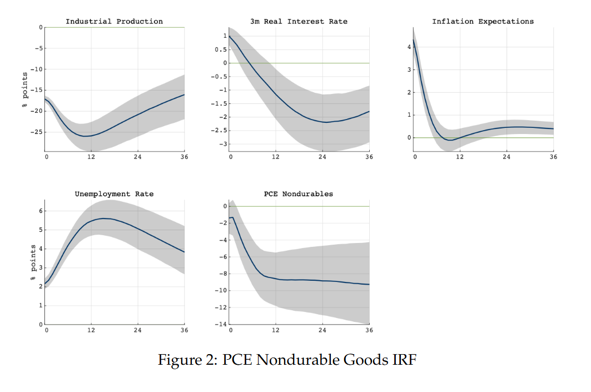

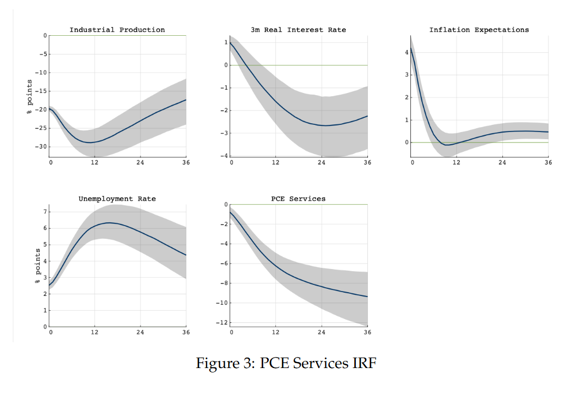

The results displayed in Figure 1, Figure 2, and Figure 3, report estimated impulse response functions (IRF) for industrial production, 3-month real interest rate, inflation expectations, and unemployment rate. The blue line depicts the IRF while the shaded gray bands present 90\% standard-error regions surrounding the point estimates.

Figure 1 reports estimates using PCE durables and displays the PCE durables IRF. The monetary policy shock leads to a noticeable initial drop in industrial production, with the lowest point occurring around the 15-month mark. A gradual recovery is observed towards the end of the period. The three-month real interest rate initially increases, followed by a significant decline, and begins to recover after approximately 20 months. Inflation expectations rise sharply at first, then rapidly decline, stabilizing around the 10-15 month period. The unemployment rate initially increases, peaking between 10-15 months, and then gradually declines. PCE durables experience an initial sharp drop, reaching a minimum around 10 months, continuing to decline before beginning to stabilize around 20 months.

The durability and lifespan of goods play a crucial role in understanding the responses. Durable goods, such as appliances and vehicles, have longer lifespans and are often considered discretionary purchases. Consequently, a shock to PCE durables might lead to a significant initial decline in industrial production as consumers delay these purchases during periods of economic uncertainty or shock. Since the production of durable goods often involves longer investment cycles and higher fixed costs, firms may reduce production significantly to avoid overproduction, leading to a steeper decline in industrial production and a slower recovery. The delayed recovery suggests that once confidence returns, the pent-up demand is gradually met. Furthermore, durable goods purchases are often financed, making them sensitive to interest rate changes. The observed increase in the three-month real interest rate following a shock can further suppress durable goods consumption, amplifying the initial decline and affecting the recovery timeline.

In the case of PCE nondurables, shown in Figure 2, the impact on industrial production is similarly characterized by an initial drop, reaching its lowest point around 10-15 months, followed by a gradual recovery towards the end of the period. The three-month real interest rate shows a slight initial increase, followed by a significant decrease, and starts to recover after 20 months. Inflation expectations also exhibit a sharp initial rise and a rapid decline, stabilizing around the 10-15 month period. The unemployment rate increases initially, peaking between 10-15 months, and then gradually declines. PCE nondurables experience a sharp initial drop, reaching a minimum around 10 months, and while they continue to decline slightly, they begin to stabilize thereafter.

Since nondurable goods include items like food and hygienic products, the goods are essential and consumed at a higher frequency. These characteristics lead to a less pronounced initial drop and subsequent stabilization across all variables but inflation expectations. Intuitively, and given that consumers demand for necessities is less elastic than services or durable goods, they are faced with making spending decisions on these products regularly. This leads to the more pronounced inflation expectations reaction. The production of nondurable goods can be more flexible and quickly adjusted to changes in demand, resulting in a less pronounced initial drop and a quicker stabilization. While nondurables are less sensitive to interest rate changes compared to durables, significant shifts in interest rates still influence overall consumption patterns, albeit to a lesser extent. The unemployment rate increases initially, peaking between 10-15 months, and then gradually declines, consistent with their more stable consumption patterns. The observed significant declines in the three-month real interest rate following initial increases suggest a delayed monetary policy response aimed at stimulating recovery. The sharp initial rises and subsequent declines in inflation expectations indicate immediate inflationary pressures followed by stabilization as the economy adjusts.

The responses to a shock in PCE services display similar patterns, as presented in Figure 3. Industrial production experiences an initial drop, reaching its minimum around 10-15 months, followed by a gradual recovery towards the end of the period. The three-month real interest rate initially increases, then undergoes a significant decline, starting to recover after 20 months. Inflation expectations rise sharply at first, then decline rapidly, stabilizing around the 10-15 month mark. The unemployment rate shows an initial increase, peaking between 10-15 months, followed by a gradual decline. PCE services see an initial sharp drop, reaching a minimum around 10 months, continuing to decline slightly but beginning to stabilize over time.

The consumption patterns in services often exhibit a mix of elastic and inelastic demand. Services like healthcare and education are essential and have inelastic demand, while discretionary services like leisure activities are highly elastic. This mixed elasticity can lead to an overall pattern that shows an initial sharp drop followed by stabilization. Service providers may have less flexibility in scaling operations up or down compared to goods producers, following the aforementioned pattern.

These results display the varied responses of economic indicators to shocks in different categories of PCE. They provide valuable insights for policymakers on the differential impacts of consumer spending on durables, nondurables, and services, highlighting the nuanced ways in which consumption shocks can influence broader economic dynamics.

V. Conclusion

This paper examines the effects of monetary policy shocks on sector-specific

consumer spending and inflation expectations using an IV-VAR framework. The

results indicate significant variations in how different sectors respond to monetary policy shocks, with durable goods showing the highest volatility in consumer spending. The pronounced initial drop in industrial production and subsequent recovery in the durable goods sector highlights the sensitivity of this sector to economic uncertainty and interest rate changes. Nondurable goods and services, while also affected, display more stable consumption patterns post-shock.

Our research emphasizes the critical role of inflation expectations in the transmission of monetary policy effects. The immediate reaction of inflation expectations to shocks, followed by stabilization, suggests that policymakers must carefully manage these expectations to avoid prolonged economic disruptions. Understanding heterogeneous sectoral responses can therefore improve the design and communication of monetary policy.

One limitation of this study is the relatively broad sector classification. Future research could incorporate more granular industry-level analysis within durable goods, nondurable goods, and services to better identify which industries are most sensitive to monetary policy shocks. Additionally, this study excludes the COVID-19 period because of the unprecedented volatility associated with the pandemic. Future research examining post-2020 dynamics could provide additional insights into how consumers respond during periods of extreme economic disruption.

Yet, our results still have significant implications for economic policy, suggesting that targeted interventions in the durable goods sector could mitigate adverse impacts of monetary policy shocks. Additionally, understanding the role of consumer behavior and inflation expectations can enhance the effectiveness of monetary policies aimed at stabilizing the economy.

Figures

References

Anzuini, Alessio, Marco J. Lombardi, and Patrizio Pagano. “The impact of monetary policy shocks on commodity prices.”В Bank of Italy Temi di discussione working paperВ 851 (2012).

Armantier, Olivier, WГ¤ndi Bruine de Bruin, Giorgio Topa, Wilbert Van Der Klaauw, and Basit Zafar. “Inflation expectations and behavior: Do survey respondents act on their beliefs?.”В International Economic ReviewВ 56, no. 2 (2015): 505-536.

Bauer, Michael D., and Eric T. Swanson. “A reassessment of monetary policy surprises and high-frequency identification.”В NBER Macroeconomics AnnualВ 37, no. 1 (2023): 87-155.

Bauer, Michael D., and Eric T. Swanson. “An alternative explanation for the “fed information effect”.”В American Economic ReviewВ 113, no. 3 (2023): 664-700.

Bernanke, Ben. “2022 Inflation Expectations: Determinants and Consequences.” National Bureau of Economic Research Conference, Spring 2022. National Bureau of Economic Research.

Cieslak, Anna. “Short-rate expectations and unexpected returns in treasury bonds.”В The Review of Financial StudiesВ 31, no. 9 (2018): 3265-3306.

Clark, Todd E., and Taisuke Nakata. “Has the behavior of inflation and long-term inflation expectations changed?.”В Economic Review (01612387)В 93, no. 1 (2008).

D’Acunto, Francesco, Ulrike Malmendier, Juan Ospina, and Michael Weber. “Salient price changes, inflation expectations, and household behavior.”В Inflation Expectations, and Household Behavior (March 2019)Мэ(2019).

Diegel, Max, and Dieter Nautz. “Long-term inflation expectations and the transmission of monetary policy shocks: Evidence from a SVAR analysis.”В Journal of Economic Dynamics and ControlВ 130 (2021): 104192.

McKay, Alisdair, Emi Nakamura, and JГіn Steinsson. “The power of forward guidance revisited.”В American Economic ReviewВ 106, no. 10 (2016): 3133-3158.

Miranda-Agrippino, Silvia, and Giovanni Ricco. “The transmission of monetary policy shocks.”В American Economic Journal: MacroeconomicsВ 13, no. 3 (2021): 74-107.

Rigobon, Roberto, and Brian Sack. “The impact of monetary policy on asset prices.”В Journal of monetary economicsВ 51, no. 8 (2004): 1553-1575.

Tversky, Amos, and Daniel Kahneman. “Availability: A heuristic for judging frequency and probability.”В Cognitive psychologyВ 5, no. 2 (1973): 207-232.